Published: 02/07/2025 By Cavender Estate Agent

Buying a home is one of the most significant financial and emotional decisions you’ll make. Understanding each stage, preparing thoroughly and partnering with a knowledgeable local agent will save you time, reduce the stress that is often involved in the process and make sure you secure the right property at the best possible price. Drawing on official guidance (GOV.UK, MoneyHelper, Citizens Advice) and Cavender Estate Agent Guildford Surrey-focused expertise, this guide delivers clear, step-by-step advice.1. Assess Your Finances and Define Affordability

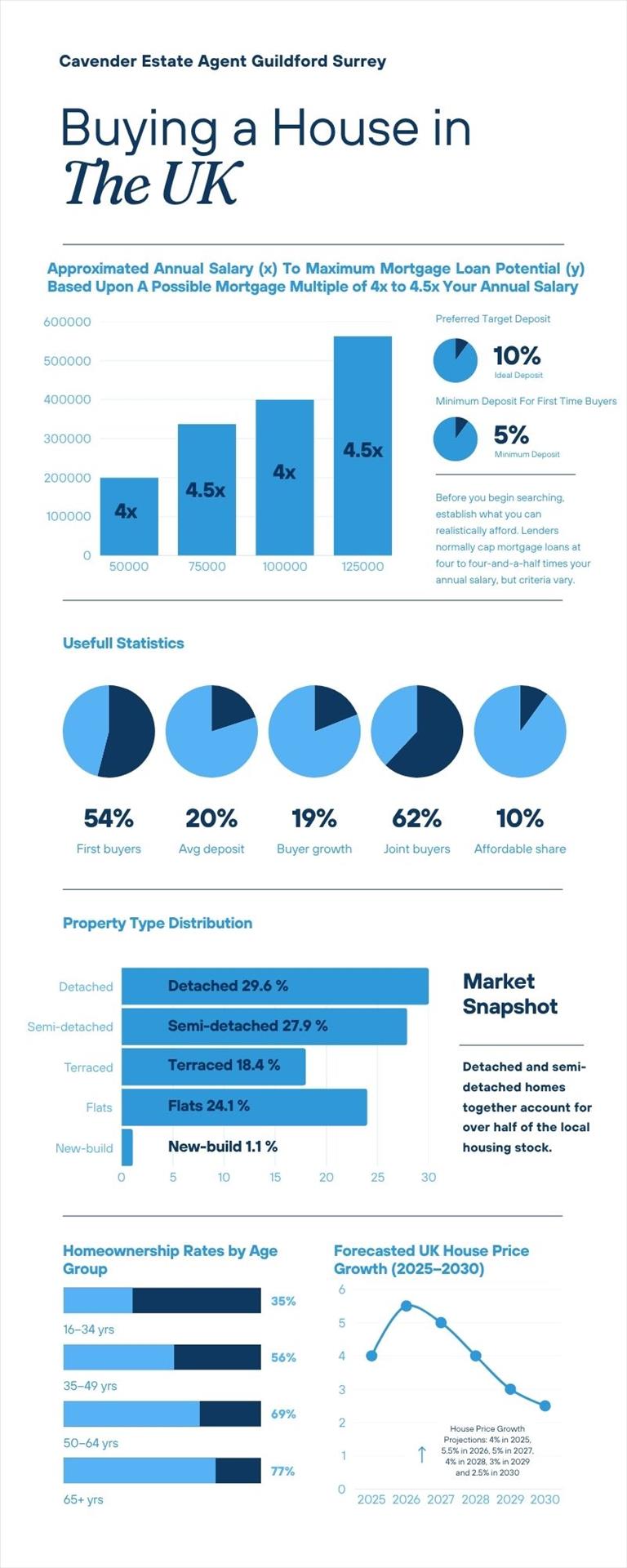

Before you begin searching, establish what you can realistically afford. Lenders normally cap mortgage loans at four to four-and-a-half times your annual salary, but criteria vary. You must factor in:- Deposit size: Typically 5–10% of the purchase price, sourced from savings, equity release or gifted deposits.

- Monthly outgoings: Council Tax, utilities, insurance and maintenance costs.

- Credit history: A clean credit record secures better rates and broader lender access.

- Additional fees: Surveys, solicitor’s fees, Stamp Duty and moving costs.

Annual Salary (£) | Mortgage Multiple | Maximum Loan (£) | 5% Deposit Target (£) | 10% Deposit Target (£) |

50,000 | 4× | 200,000 | 10,000 | 20,000 |

75,000 | 4.5× | 337,500 | 16,875 | 33,750 |

100,000 | 4× | 400,000 | 20,000 | 40,000 |

125,000 | 4.5× | 562,500 | 28,125 | 56,250 |

Use Cavender's online mortgage and affordability calculators for personalised estimates. Our in-branch broker referrals will compare deals, verify your borrowing capacity and secure a Decision in Principle, demonstrating to sellers that you are financially prepared.

2. Secure a Mortgage in Principle and Explore Buyer Schemes

A Mortgage in Principle (MiP) is an agreement from a lender confirming the amount they would loan based on your income, credit profile and deposit. It typically lasts 30–90 days and may involve a small booking fee. Having an MiP in place:- Strengthens your offer.

- Prevents disappointment should you make an offer beyond your borrowing potential.

- Highlights your seriousness to sellers and estate agents.

- Help to Buy: Equity Loan: Available on new-build homes up to £600,000 (England). The government lends up to 20% (40% in London) interest-free for five years.

- Shared Ownership: Buy a 25–75% share of the property, paying rent on the remainder. Staircase (increase share) over time.

- First-Time Buyer Stamp Duty Relief: No Stamp Duty on properties up to £425,000; reduced rates up to £625,000.

3. Define Your Search and View Properties

With finances in order, clarify your property criteria. Consider:- Location: Core focus on Guildford, Kingston upon Thames and surrounding Surrey towns (Godalming, Woking, Cranleigh).

- Property type: Freehold house, leasehold flat, new build or period conversion.

- Size and features: Bedrooms, garden, off-street parking, proximity to schools or transport links.

- Energy performance: EPC rating of C or above is ideal for efficiency and future resale value.

- Local market intelligence (average sale prices, demand trends).

- Regular access to Rightmove, Zoopla and our pocket listings.

- Accompanied viewings with detailed area insights.

- Structural condition: look for cracks, damp or subsidence indicators.

- Neighbourhood ambience: noise levels, traffic, community facilities.

- Boundaries and fixtures: verify what is included in the sale and any potential maintenance liabilities.

4. Make an Offer and Arrange Surveys

Once you identify your preferred property, submit an offer “subject to contract”. This protects you until both parties exchange written contracts. Consider:- Offer level: Base it on recent local comparables, time on market and condition issues uncovered during viewings.

- Subject to survey: Ensures renegotiation if structural concerns arise.

- Holding deposit: Often £500–£1,000, refundable if the sale falls through for reasons beyond your control.

- Mortgage valuation survey: Required by lenders to confirm property value; cost typically £150–£300.

- HomeBuyer Report or full structural survey: Detailed condition assessment; ranges from £400 to £1,000 depending on property age and type.

5. Conveyancing and Legal Due Diligence

Conveyancing transforms your offer into a legally binding contract. Key steps include:- Engage a solicitor or licensed conveyancer: Obtain transparent quotes covering fees, disbursements, VAT and estimated Stamp Duty.

- Local searches: Essential checks include local authority planning, environmental risks, water and drainage. Costs typically range from £250 to £400.

- Contract review: Confirm property boundaries, restrictive covenants, rights of way and fixtures included in the sale.

- Deposit preparation: Usually 10% of the purchase price, held by your solicitor in a client account.

6. Exchange Contracts and Plan Completion

Exchange marks the point at which the agreement becomes legally binding for both parties. To prepare:- Review final draft contract and schedule of fixtures.

- Confirm mortgage offer is in place.

- Ensure deposit funds are available for transfer.

- Agree a completion date convenient to all parties.

- Buildings insurance must commence from the completion date.

- An estate agent will circulate a completion checklist detailing any last-minute actions.

7. Completion and Beyond

Completion day is when funds transfer, keys are released and you become the legal owner. Following completion:- Land Registry registration: Your solicitor will register the title with HM Land Registry and pay the Land Registry fee.

- Stamp Duty Land Tax (SDLT) or Land Transaction Tax (LTT): Pay within 14 days (England & Northern Ireland) or 30 days (Wales). Late payment incurs interest and penalties.

- Utilities & Council Tax: Notify suppliers and the local authority of your move-in date.

- Moving logistics: Coordinate removal firms, parking permits and childcare as needed.

- Transfer of council and utility accounts.

- Introduction to our preferred maintenance and decorating partners.

- A complimentary neighbourhood welcome pack, detailing schools, shops and transport links.

8. Why Choose Cavender Estate Agents?

When complexity meets local nuance, you need more than a national portal. Cavender stands out through:- Dedicated Surrey expertise: Two offices in Guildford and Kingston upon Thames, covering Godalming, Woking, Cranleigh and surrounding commuter belt.

- Full-service offering: Sales, lettings, valuations, mortgage support, conveyancing referrals and property management under one roof.

- Transparent fees: No hidden charges, clear disbursement breakdowns and competitive commission rates.

- Client-Money Protection: Fully insured client accounts satisfy Propertymark regulations.

- Community engagement: Sponsorship of local schools, charity cycles and area guides that deepen our neighbourhood connections.

9. Frequently Asked Questions

Question | Answer |

What deposit do I need? | Aim for at least 5% for a standard mortgage; 10% broadens lender choice and secures better rates. |

How long does conveyancing take? | Typically 6–12 weeks from offer acceptance to completion, depending on search times and solicitor workloads. |

Can I include fixtures in the sale? | Yes. Negotiate items such as carpets, curtains and light fittings; ensure they are listed in the contract schedule. |

What happens if searches reveal issues? | You may renegotiate the price or request seller-paid remedial works. Your surveyor and solicitor will advise on material concerns. |

Do I need buildings insurance before exchange? | Only upon completion. However, some buyers choose to arrange cover from exchange to guard against unexpected delays. |

Is Stamp Duty due on a second home? | Yes. An additional 3% surcharge applies to second properties. |

10. Next Steps

- Calculate affordability using our online tools.

- Book a free valuation with a local Cavender expert.

- Secure your MiP by completing a brief income and expense questionnaire.

- Register your search criteria for instant property alerts.

- Read our First-Time Buyer Guide for a detailed walkthrough of government schemes and local insights.